NOR; Why deduct reimbursable AND non-reimbursable expenses?

It seems multiple sources are stating that the Net Operating Revenue "represents the net dollars remaining after deducting the invoiced consultant's fees and expenses; AND all non-reimbursable AND reimbursable project-related expenses." AHPP pg 410

My question is, by definition reimbursables are in fact paid back to the firm (with a mark-up for profit even) why are they deducted from the revenue?

Thank you so much!

-

Received my answer - thank you AmberBook!

The markup [on reimburseables] isn't really for profit, it's just to cover the administrative expenses associated with the activity. There are minor accounting expenses associated with moving those reimbursable expenses around.

That would be why you wouldn't want to include reimbursables in your revenue, while technically you're getting paid back for those copies you made, or fuel you used to get to the job site, the monies you're receiving plus a 10% markup, (or whatever that percentage might be) is really a small amount towards the effort accounting puts in to track those. -

I don't know what the answer was that Jennifer Hicks received from AmberBook but it seems to me that the definition of Net Operating Revenue on p.410 of the AHPP is wrong.

Net Operating Revenue (AHPP p.410)

Represents the net dollars remaining after deducting the invoiced consultant's fees and expenses, AND all reimbursable and non-reimbursable project-related expenses.

Reimbursable and non-reimbursable expenses should NOT be deducted from the gross revenue to find the net operating revenue.

Can anyone confirm this?

-

Citrillion,

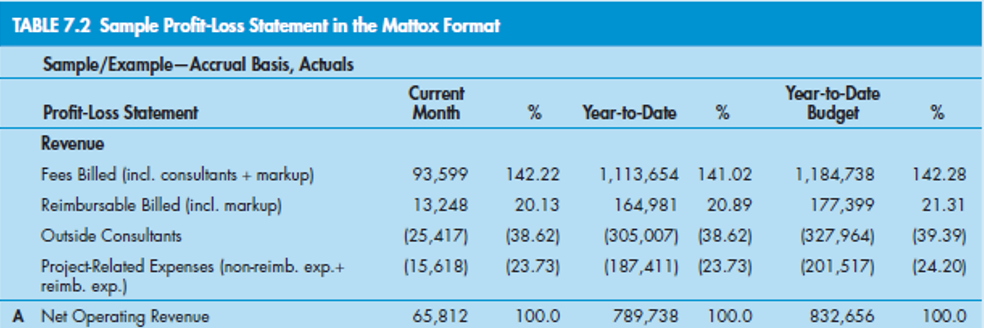

If you look at the Revenue section of the P&L Statement in Table 7.2 on p. 424 of the AHPP, you will notice 4 line items:

1. Fees Billed (incl. consultants + markup)

2. Reimbursable Billed (incl. markup)

3. Outside Consultants

4. Project-Related Expenses (non-reimb. exp.+ reimb. exp.)

1 & 2 are asset items, whereas 3 & 4 are liability items. The sum of all these 4 items generates the Net Operating Revenue (NOR). As can be clearly seen, on the contrary to what Jennifer Hicks have mentioned above, the markups on both the consultant fees and the reimbursable fees are included in the NOR. Item #3 is the consultants' invoices to the firm, and Item #4 is the project-related expenses without markup (pure expenditure) derived from both the cash- and accrual-basis accounting tables. Basically, you punch in your invoices (assets), stripe the expenditures (liabilities), and leave the Net Operating Revenue.

Hence, what's described for the NOR in the AHPP on p. 410, "Represents the net dollars remaining after deducting the invoiced consultant’s fees and expenses, and all reimbursable and non-reimbursable project-related expenses.", is correct.

If you deduct only the consultants' fees from the gross revenue generated by the design + reimb. invoices to the client, that's called Net Service Revenue (AHPP p. 636). Hence:

NOR = NSR - Non-reimbursable Expenses

-

Citrillion,

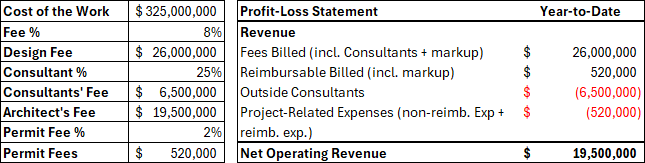

Marketing and promotion expenses are not project-related; they are part of the firm's overhead as indirect expenses and therefore are not included in NOR. Permit and AHJ fees, on the other hand, are truly project-related expenses paid by the architect in advance and invoiced to the owner if such is stated in the B101; these reimbursable fees are "generally/professionally" not marked up. They are included in the NOR calculation, but because their +/- difference will be net zero ($0 because it's all-in and then all-out), they have no effect (as explained in the Hyperfine document). Hence:

If the question had stated that "...the architect will have a 10% markup with respect to his administrative efforts for getting the required permits...", then the NOR would be:

$19,500,000 + ($520,000 x 10%) = $19,552,000

Just because the Reimbursable Billed (incl. markup) asset item figure would appear as $572,000 in the P-L Statement:

$572,000 + ($520,000) = $52,000

-

Thank you LeventK!

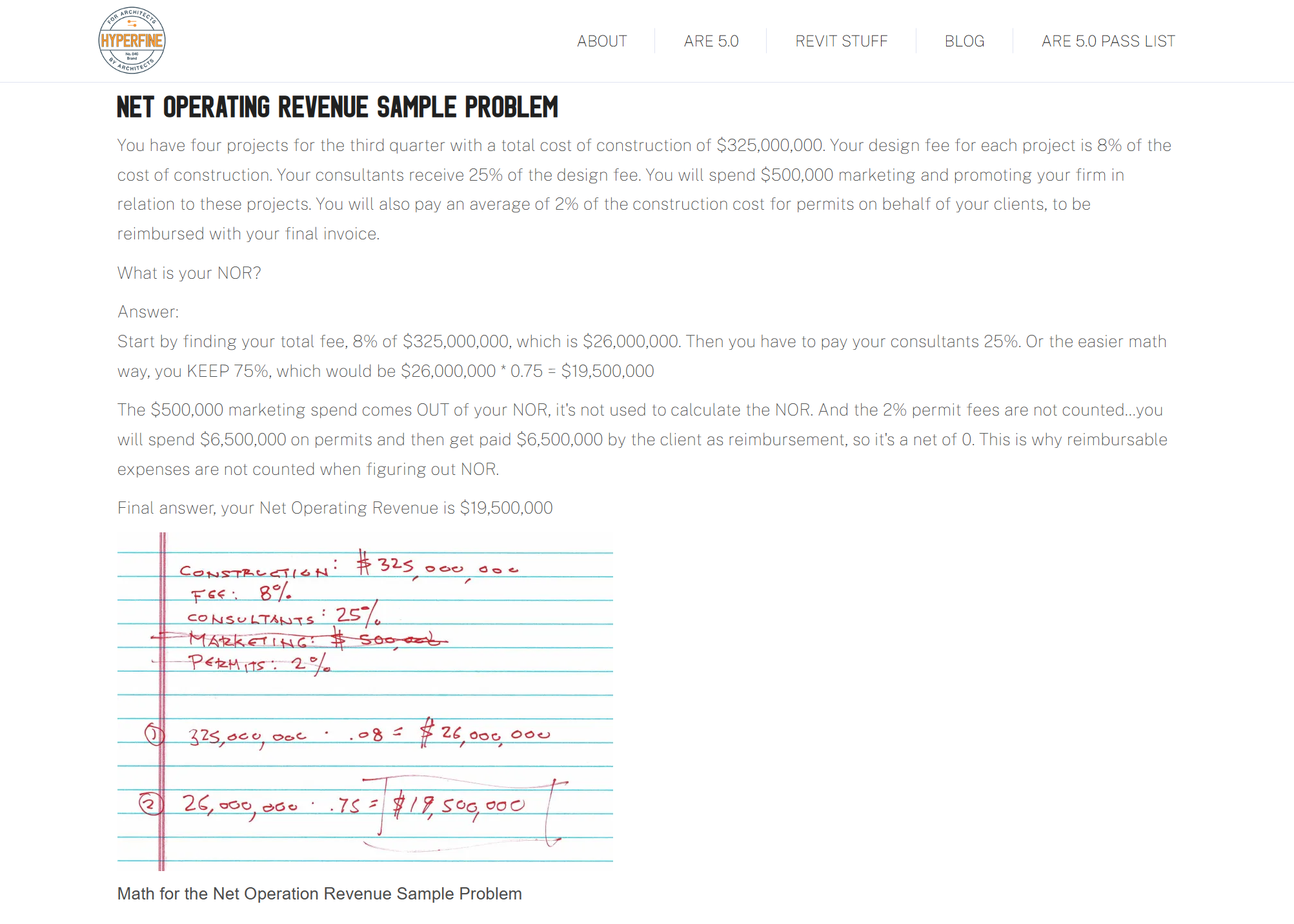

I understood that reimbursables, in this case the permitting fees SHOULDN’T be included BECAUSE they cancel out and amount to $0. But now I understand that they SHOULD be included, as a matter of accounting, EVEN IF they cancel out and amount to $0 or in the event that there is a markup, in which case the markup would count toward the NOR.

I was also confused because in Hyperfine’s explanation he says, ‘…you will spend $6,500,000 on permits and then get paid $6,500,000 by the client as reimbursement, so it’s a net of 0. This is why reimbursable expenses are not counted when figuring out NOR.’ In fact, reimbursable expenses ARE counted (per the AHPP definition) even if they have a net value of 0. I suppose this is useful to keep track of cash flow on the P-L statement.

I was tripped up by the wording ‘in relation to these projects’. I took this to mean that the $500,000 marketing and promotion expenditure was a ‘project related expense’ and therefore SHOULD be included in the NOR calculation. Barring this tricky wording, I do see that marketing and promotion in and of themselves are indirect expenses and SHOULD NOT be included in the NOR calculation.

Thank you for taking the time to help me understand this question.

-

Citrillion,

Glad to hear that you've solved the mystery. Happy to be helped of. Cheers. I may add a small reminder here: please note that reimbursable expenses are not included when evaluating Overhead Expense to calculate the firm's Break-Even Rate.

Overhead Expense = Total Indirect Expense + Total Indirect Labor

The $500K marketing and promotion expense above enters into play just here.

Please sign in to leave a comment.

Comments

8 comments