Reimbursable expense- PJM

Do we deduct reimbursable expense from the Net Service revenue to find the total architect's fee left to pay for labor/ salaries? The NCARB question states non-reimburable that I understand we need to deduct, but what about reimburable expense?

NCARB practice exam question:

An architect is preparing an initial project budget using the following fee information:

- There is a total fee of $300,000 for the entire project team.

- 40% of the total fee is allocated for all consultants.

- 8% of the net fee is allocated for the architect's non-reimbursable expenses.

- 7% of the net fee is allocated for the architect's contingency.

What is the available budget for project labor?

-

Reimbursable expenses would not be a net gain or a net loss. They're expenses that are attributed to the project spending (for example: you have a project that includes food cost, travel cost, lodging cost, and other related work expenses for a billable job) and gets billed to the owner. Non-reimbursable expenses, typically overhead items that relate to project management, operations, etc., are included because those eat into the take home pay for the architect for the project, since they cannot seek reimbursement for them from the client or anyone else.

-

300,000 is the total fee for the whole design team. 40% of that is allocated to consultants, leaving 180,000 for the architect. The reimbursable expenses are, typically, in addition to the standard fee as they're just that: additional expenses related to the project.

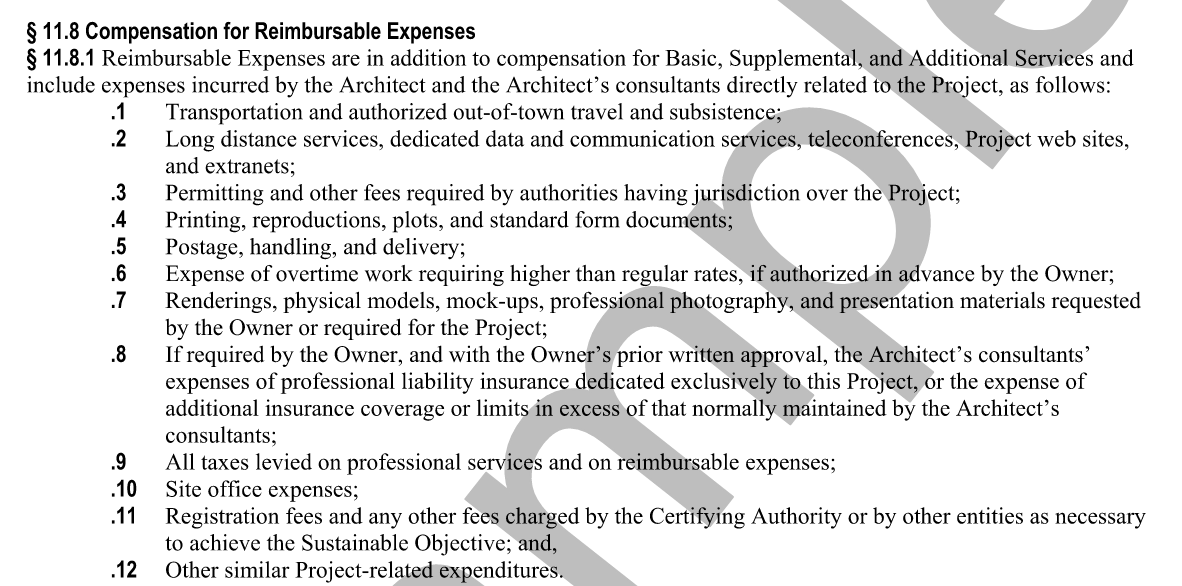

See Section 11.8 from the standard B101 agreement below:

-

Non-reimbursable expenses dig into the profit on the project as overhead costs of project operation. Contingencies are in place to help mitigate unforeseen risks or issues that can/will arise on a project.

These two costs would eat into the final take home revenue of the architect, and could be foreseen and appropriate to account for in their fee. Typical reimbursable expenses such as airfare, lodging, etc. are not part of the basic scope of services to complete the work of SD/DD/CD/CA aside from the agreed site visits required during CA, etc. They are apart of additional services and project investigation that was not included in the original agreement.

Example: an architect from NH has to visit AZ for a couple of days per request of the owner for site investigation. Their flight, hotel, car, and meals comes out to 1.4k in total. The architect pays that 1.4k out of pocket, and it is then billed to the owner for the same amount as an additional project cost. It's a net neutral because it's reimbursed and is not a gain or loss in cost/revenue for the architect.

-

Reimbursables are expenses paid by the architect on behalf of the owner. In order to avoid dispute as to what constitutes overhead and what is a reimbursable expense, the agreement should itemize the types of expenses for which the owner will pay, including the amount of any mark-up that the architect is entitled to for advancing such costs. B101, Section 11.8.1 lists compensation to the architect for reimbursables, including transportation and authorized travel and subsistence, long distance services. Some architects do not claim transportation as a reimbursable expense except for out-of-town travel. The decision of whether travel expenses should be billed as reimbursables should be made on a project-by-project basis, taking into account the value of building and retaining good will with the owner.

B101, Section 11.8 defines and lists reimbursable expenses. It includes as a reimbursable the expense of additional insurance coverage requested by the owner in excess of that normally carried by the architect and his consultants. However, owner opposition is likely to be strong if the architect carries little or no professional liability insurance. There is a growing trend for the owner to bear the cost of that insurance. Probably, the better view is for the owner and architect to select whether the architect=s insurance is reimbursable on a project-by-project basis. -

1. Consultant fee: 40% x $300,000 (total fee) = $120,000

2. Net fee: $300,000 - $120,000 (consultant fee) = $180,000

3. Non-reimbursable expenses and contingency: 15% x $180,000 (net fee) = $27,000

4. Total available for labor: $180,000 (net fee) - $27,000 (combined percentage of fee for contingency and non-reimbursable expenses) = $153,000

Please sign in to leave a comment.

Comments

9 comments